Despite high Transport Capacity - Why the Situation in Europe differs from 2023

Market Monday - Week 12 - A seasonal decrease in road transport capacity is monitored. But what makes this year different from 2023 and what implications does it have for the rest of the year?

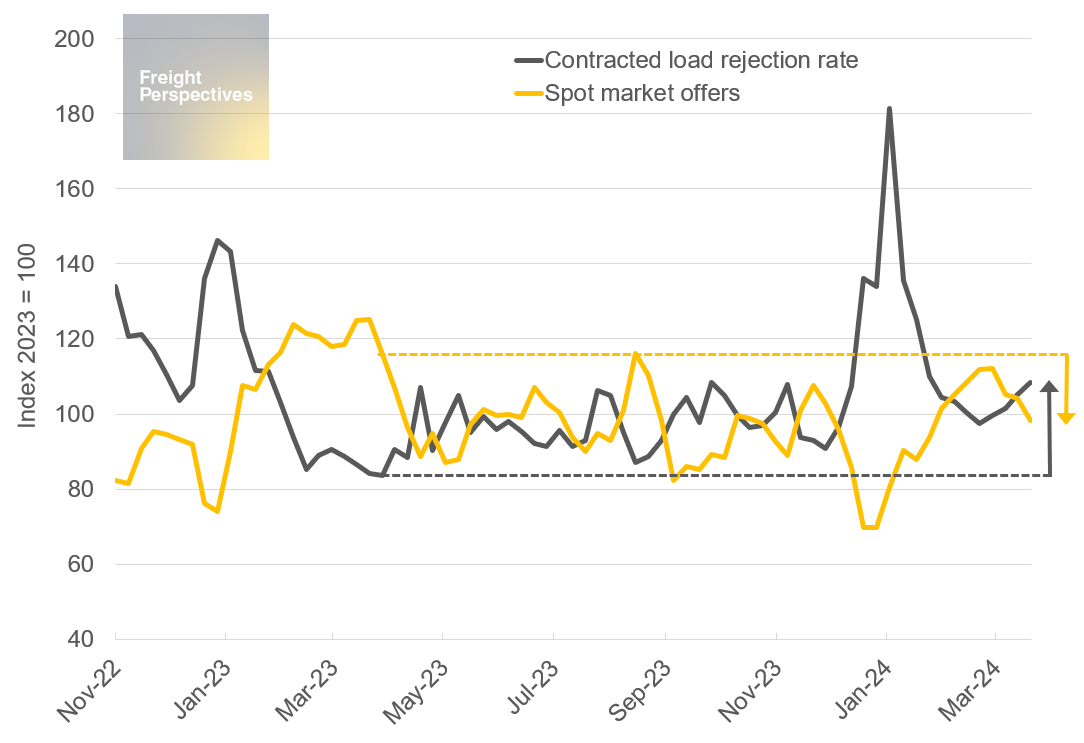

In this episode of Market Monday I’ve examined the expected seasonal trends of contracted load rejections (transports that are either timed out or rejected by carriers) and offers on the spot market. These two KPIs are our main measures of short-term available truck capacity in the market. Typically, as we approach Easter, rejections increase and offers on the spot market decrease. Although at first glance, the overall figures seem to align with expectations and the last year`s data, a closer look reveals significant differences.

Capacity KPIs - measuring European market behavior

Source: Transporeon Market Insights, own calculation and illustration

In 2023, at the same time (not in exact date but in weeks prior to Eastern) we faced a different situation. Both metrics showed different levels of available capacity. However, in week 11 of 2024, we see an increase in rejections (+24 index points) and a decrease in offers (-17 index points), representing a significant shift from the previous year.

As a consequence, we should anticipate a further increase in contracted load rejections and a decrease in spot offers during the Easter period, as this seasonal movement just started. This suggests that due to increased rejections, I expect more ad hoc and urgent shipments directed to the spot market compared to 2023, which will further drive up spot rates in the coming weeks.

While demand for transportation remains around last year’s levels, changes in capacity primarily caused this altered situation. Reduced fleets and the reallocation of trucks to other business areas (such as regional and local business instead of international spot market) seem to be the main reasons for this development.

If so, we should prepare for further decreases in capacity and increases in rates throughout 2024.

Christian Dolderer

Lead Research Analyst