European’s Road Spot Market Offers are down 18%

Market Monday - Week 24 - Compared to 2023 offers are down by 18% and main contributor to recent high spot prices.

One month ago, I shared my view on the available capacity in Europe, highlighting contracted load rejections (transports that are either timed out or rejected by carriers) and spot market offers. These two KPIs serve as our main indicators for short-term available truck capacity in the market. Typically, rejections increase and offers decrease when capacity is reduced.

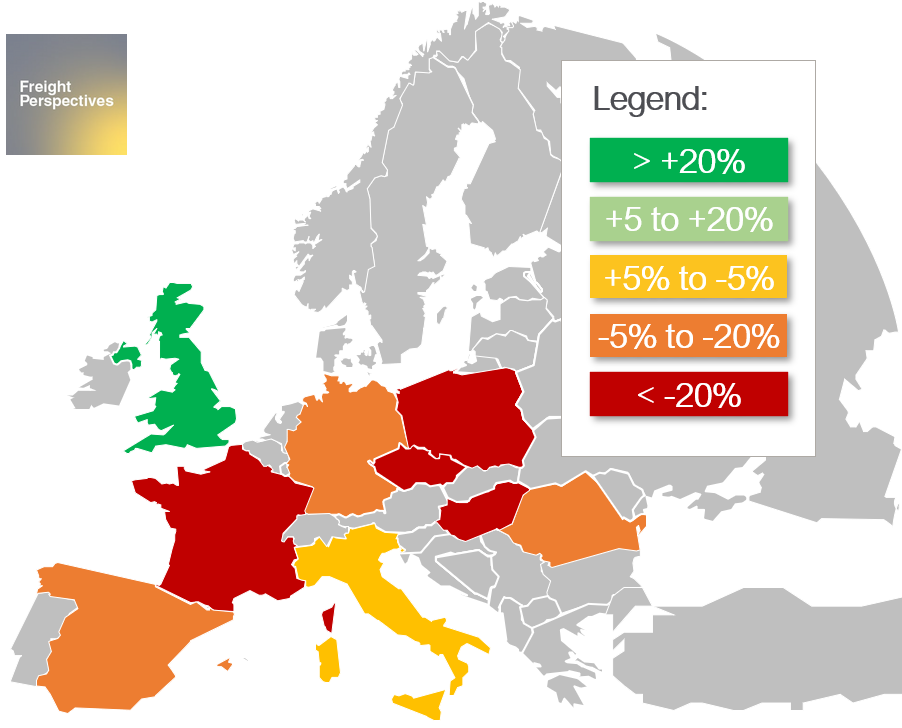

After evaluating the rejections in more detail last month, today I will drill down into the offers. The following map highlights the countries most affected by changes on the spot market. France, Poland, Czechia and Hungary faced the highest decreases, while Germany, Romania and Spain also saw significant reductions.

Comparison of offers on the spot Market between weeks 1-22 of 2023 and 2024

Source: Transporeon Market Insights, own illustration and evaluation

Italy maintained a stable situation, contrary to the overall trend, whereas the United Kingdom demonstrated its independence from the overall European transport market situation.

This trend also applies to international transportation in Europe, with the number of offers down by 19,3% compared to the same period last year.

What implications does this have for the market now and in the coming weeks and months?

A reduction in offers on the spot market indicates a decreased available capacity for this market segment. Likely contributing factors include the low prices over the past year and a half, making this market less attractive for carriers. A further fundamental explanation could be that spot market focused carriers have considerably downsized their fleets or changed their business model. The recent surge in bankruptcy announcements further contributes to this.

This situation lays the groundwork for the substantial spot price increases we’ve monitored recently. Fewer offers mean less competition, leading to a rise in spot prices. In addition, detailed analyses on the data reveal that in Poland, Czechia and Germany also “last minute” spot transports almost doubled. These ad hoc spot market requests, typically resulting from unsuccessful attempts at contracted market assignment, usually translate into higher transport prices than an initially planned spot transport.

If this trend continues, combined with a possibly accelerating demand increase, spot prices are likely to remain high and may even rise further throughout the year. On the other hand the situation in 2022 also showed that if spot prices reach and remain on an attractive level, carriers are likely to start relocating their fleets to the spot market to capitalize potentially higher margins. This could then initiate a counter-movement mitigating further spot price increases.

In the short-term, I expect spot prices to remain above contracted rate levels due to the reduced competition in this segment. In the mid-term, the overall situation will determine whether we`ll see further increases based on a return to a growth economy.

If you are interested in a condensed update on how the market evolved combined with the current state of alternative fuels and how they’re impacting road transportation?

Than please join us on June 18th at 13:00 CET for our live webinar:

Christian Dolderer

Lead Research Analyst