Shortened Rest Period Index Highlights Operational Pressures in 2024

Market Monday - Week 48 - New KPI reveals growing driver shortages as carriers push rest period limits to meet market demands

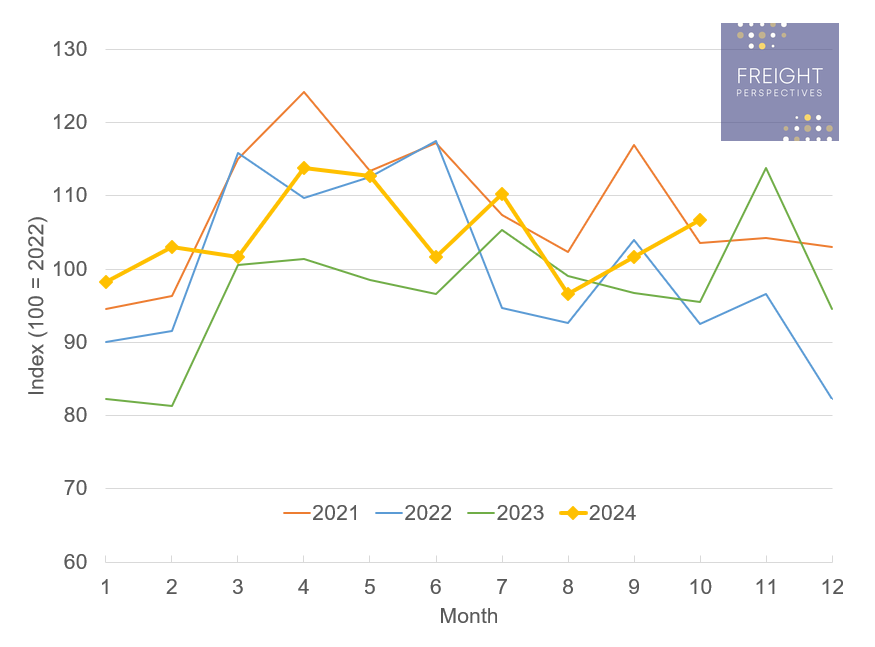

In these volatile times, available capacity is the most pressing topic in the transport market. It is the perfect moment to introduce a new Key Performance Indicator (KPI) that we have been using in the background for months in our interpretations and assessments - the Shortened Rest Period Index. This KPI measures the shortened weekly rest times taken by drivers within a month.

According to EU regulations, drivers can take a reduced weekly rest period of at least 24 hours instead of the regular 45 hours, provided that the reduction is compensated by an equivalent period of rest taken en-bloc before the end of the third week following the week in question.

This flexibility allows transport companies to better manage their schedules, meet delivery deadlines, and improve operational efficiency temporarily while still ensuring that drivers get adequate rest to prevent fatigue and maintain road safety.

This KPI is based on Transporeon real-time visibility data, allowing us to review the operational pressure in a market environment.

European index of shortened rest periods taken

Source: Transporeon Real-Time Visibility

Values above 100 indicate a market situation that required a higher usage of shortened rest periods than the average situation in 2022. Typically, the very busy and hectic months within a year show the highest values, representing a seasonality that can be seen in this chart.

What becomes clearly visible in this data is that in 2023, a year with overall high capacity supply, the need for shortened rest periods was low compared to other years. Now in 2024, we see a different picture, clearly departing from the levels of 2023 and aligning more closely with 2022 and 2021.

Outstanding is the situation in the last month (October) with a record high utilization of shortened rest periods. This could be interpreted as:

the market required a high capacity provision

prices, at least on the spot side, were attractive

dispatchers/employers were willing to order their drivers to execute them

This data also proves that from an operational perspective, currently, carriers utilize their available assets (fleet and drivers) close to its maximum, leaving only a theoretical possibility for a rather relaxed capacity situation during the year-end peak season.

Christian Dolderer

Lead Research Analyst

Transporeon