What’s Driving Czechia’s Spot Transportation Costs?

Market Monday - Week 27 - Whats impacting international lanes involving Czechia: Market dynamics, regulatory changes or something different?

Over the past three months, a trend analysis of Market Insights showed that transportation routes involving Czechia led the board for changes in spot prices. For example, the rates from Austria to Czechia increased by +39.1%, and the rates from Czechia to Great Britain rose by +26.8%. These are just two corridors demonstrating high percentage changes compared to week 13. This prompted me to examine the details to understand whether this is a major shift of market dynamics or a result of regulatory changes. Therefore, I divided all the routes involving Czechia into two clusters (outbound & inbound) to see if this is a general trend or if we can explain it by an imbalance effect, for instance.

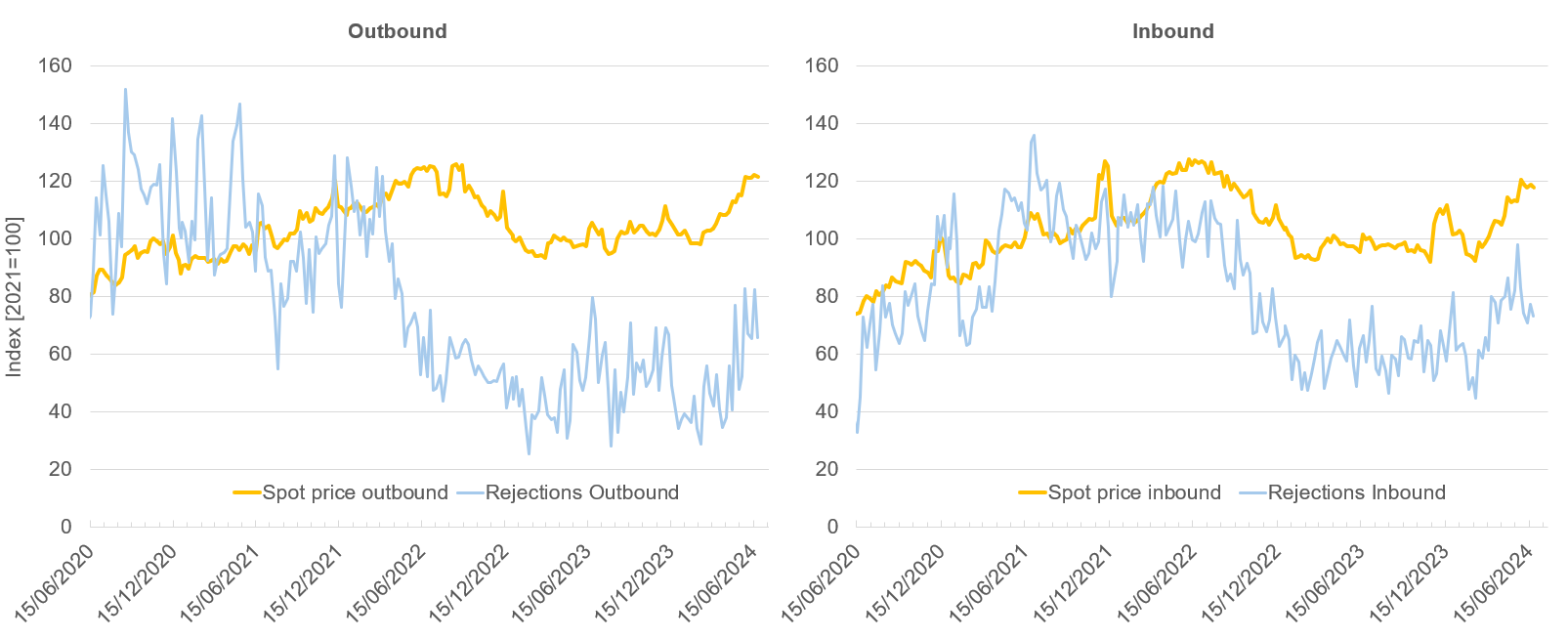

Comparison of inbound and outbound lanes in Czechia

Source: Transporeon Market Insights, own illustration and evaluation

The chart comparing in- and outbound lanes suggests that an emerging imbalance is not the cause of the recent price increases. The contracted load rejections serve as a second indicator, primarily reflecting the supply side. This KPI has shown a noticeable increase over the last three months. However, this alone does not explain why spot rates reached peak levels again in 2022. The rejection index values around 80 suggest a different situation compared to 2021 (Index 100) and 2022. Although clearly impacting, it can’t be the only explanation for the spot rates reaching 2022 peak levels again. If we examine the major cost components, the current diesel prices are considerably lower than they were in 2022. This increase in the gap requires an explanation.

I have two main theories for this situation. First, spot prices on these routes could be more affected by other cost components like tolls and driver wages than before. This is somehow odd because spot prices usually are less cost sensitive and are more subject to demand & supply fluctuations. Second, even small supply changes (compared to 2022) could be causing large price increases. This would suggest that there´s less available capacity overall and particularly on the lanes involving Czechia than I initially thought.

I don't have a definitive answer yet, so I'm asking YOU our community for your thoughts and comments.

Do you see something that could be significantly affecting the situation that I may have overlooked in my analysis?

Christian Dolderer

Lead Research Analyst