Are carriers withdrawing Eastern Europe based trucks out of Western Europe?

In recent weeks, I received this particular question several times, including our Freight Perspectives Webinar on June 18th. If it were true, it would explain many of the market situations and reactions we’ve observed. Various reports suggest this, citing high bankruptcies figures and fleet reductions as responses to low market prices, increased production costs, and administrative hurdles such as the mobility package. I`ve previously discussed this new situation, which involves monitoring rejections and offers, and its particular impact on the spot market and associated prices.

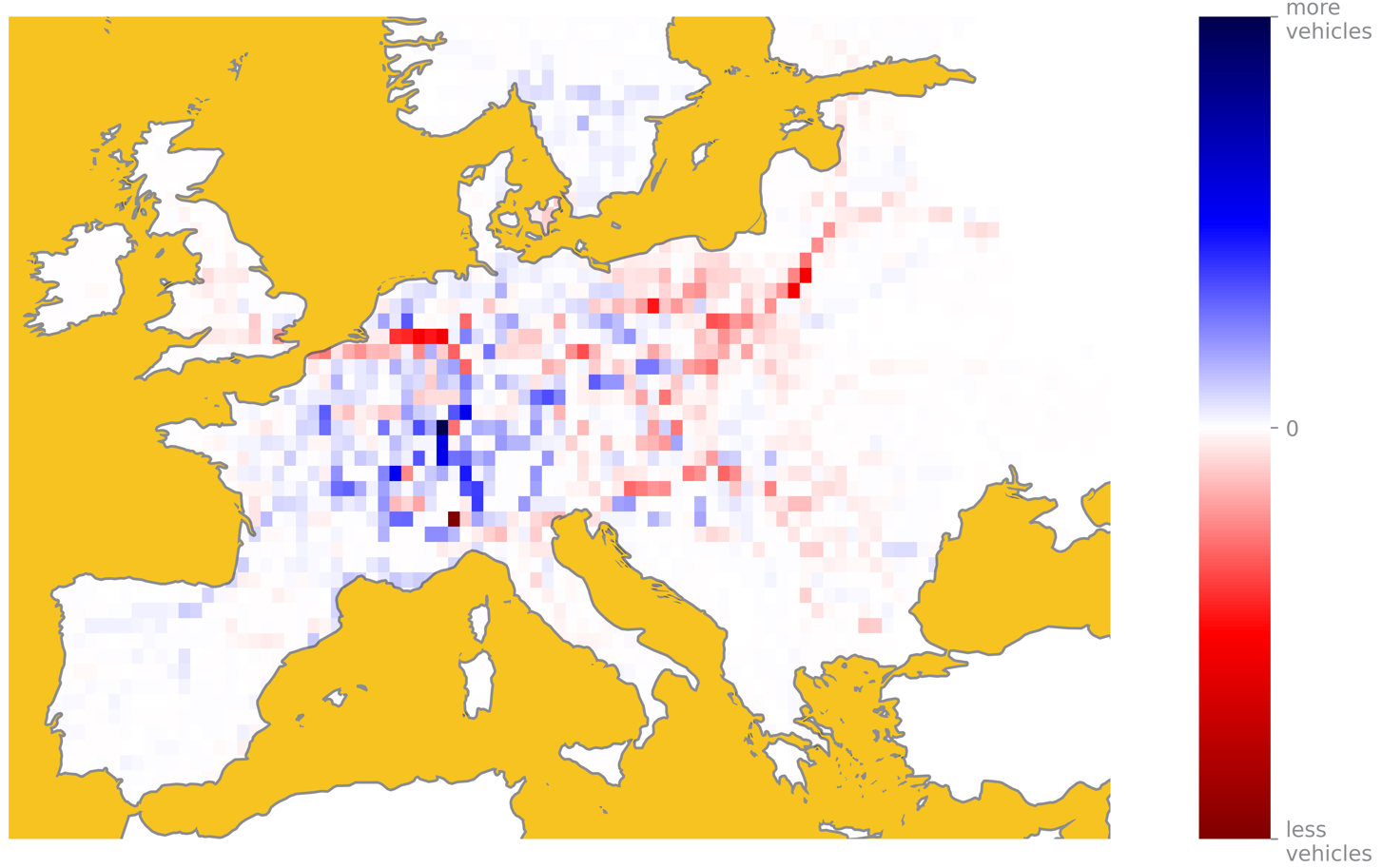

We’ve begun exploring how we can investigate whether such a movement or withdrawal, intentional or otherwise, exists and can be measured. We performed different approaches using Transporeon platform data. However, the results were neither supporting nor rejecting the hypothesis. I will share the results of one of these attempts, as it best describes the current situation. The following graphic, based on our real-time-visibility data, compares the activity of Eastern Europe based trucks in February and May of each year. Our choice of these months is based on customer feedback indicating a change around Easter that has continued since.

Comparison of fleet movements from February to May among Eastern European carriers

Source: Transporeon Real-Time-Visibility

Each year tells a unique story and effects deriving from covid restrictions and Russian invasion into the Ukraine affected each year. However, what sets 2024 apart is the high number of red pixels, especially in France, Belgium, and Italy. Based on this analysis, we can reasonably assume that fewer trucks from Eastern Europe were active in these regions in May compared to February. Does this confirm the theory that these trucks have been withdrawn from these regions? Not necessarily, as it just compares points in time and ignores general effects such as growth over a certain period of time or shift in demand patterns. A year-over-year analysis could provide this confirmation. The next chart shows the comparison of May 2023 with May 2024.

Comparison of fleet movements in May 2023 vs 2024 from Eastern European carriers

Source: Transporeon Real-Time-Visibility

The unsatisfying answer is that year-over-year analyses using various time periods do not confirm a general withdrawal. In France, compared to 2023, there is instead an increase in the number of trucks based in Eastern Europe visible. We normalized data to account for fleet size changes and platform effects.

So, what additional factors could be influencing the current market situation in 2024?

Potential explanations include demand increases indicating a return to a growth economy in the affected regions (e.g. France, Italy). Alternatively, it could be attributed to “bad luck”, such as the fleet not being in the regions that needed it most in recent weeks. Also an overall decrease in efficiency or utilization of the trucks should be named as influential factors.

While fleet reductions and withdrawals may contribute, we can’t definitely confirm them as the ultimate reasons.

Generally, the fleet can be best described as a fluent and permanently adjusting organism. This becomes evident when inspecting the European road transportation market over time. Therefore, comparing different time frames is extremely challenging as the underlying fundamentals float. Even more, predicting future fleet movements is almost impossible, especially over longer periods.

Currently, some cross-border transportation markets are showing a significant increase in contracted load rejections and consequently, elevated spot prices. We will continue to closely monitor this situation, particularly if there is a substantial and consistent demand increase that further heats up the situation.

Christian Dolderer

Lead Research Analyst